Surviving a Bear Market

Surviving a Bear Market

Originally published 10/28/22: The current economic environment is testing the discipline of even the savviest of investors. Some may panic and jump ship, while others will ride it out and wait for calmer waters. Which mindset do you have?

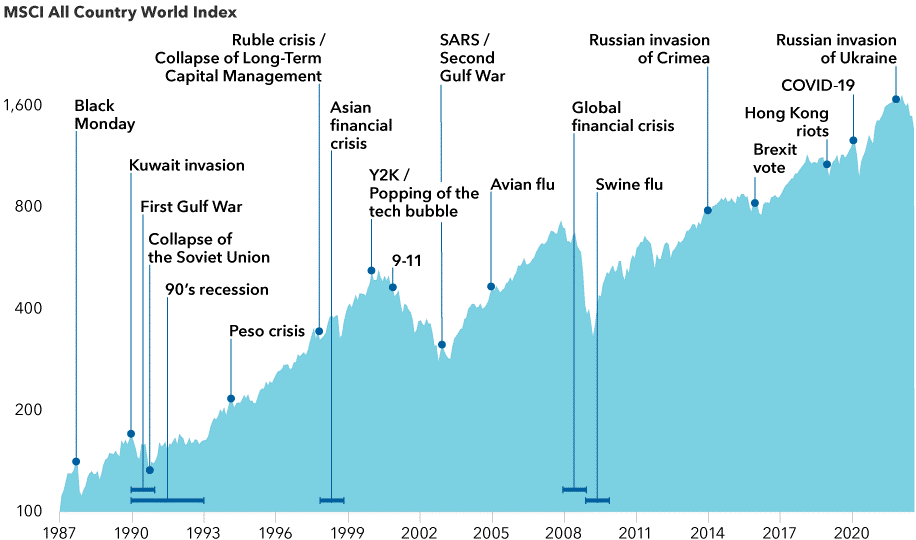

All markets move in cycles, including periods of steep contraction. Since equity markets have reached multiple record highs over the last few years a downturn was inevitable. But, if the term “bear market” scares you, here are some facts to put it in

perspective:

• Bear markets are normal. Since its inception in the late 1920s, the modern S&P 500 has seen 26 bear markets – stocks lost 36% on average. During that same time long-term investors were rewarded with 27 bull markets where stocks gained an average of 114%.*

• The average frequency between bear markets is 3.6 years. You could see about 14 bear markets during a 50-year investment window. Since 1930, the market has been bearish for a time equal to 20.6 years. This means that stocks have been on the rise the other 71.4 years!*

• Bear markets last for significantly less time than bull markets. Bears last on average 9.6 months. Bulls last on average 2.7 years.*

*Source: cnbc.com; 6/13/22

These are challenging times, but the markets have historically proven remarkably resilient over the long term. Stick with your well-diversified, long-term financial plan, partner with a trusted financial advisor, and keep inflammatory headlines in perspective to stay on course toward your financial objectives.

Author: Jill Mollner, MBA, CFP®

Wealth Advisor, RJFS

Branch Operations Manager

Does your advisor review your investments daily?

Our advisors review fund performance daily, weekly, and monthly. And our Investment Committee systematically tests and replaces positions in advisory accounts that no longer meet our standards. This diligence is especially important in volatile markets.

Do you meet with your advisor at least once a year?

What do you talk about? These meetings should be more than just a chance to catch up. Have market conditions thrown your investment strategy off-track? How do recent life events affect your estate plan? Do new tax laws affect you? We meet with clients at least once each year, and more frequently based on their needs.

NOT A CORNERSTONE CLIENT?

Given today’s environment, getting a second opinion about your plan could help you make smarter decisions. Just like you, our clients want to be able to enjoy life and take care of the people they care about. They look to us for help living the life they’ve imagined no matter what is happening in the financial markets or economy.

Call 605.357.8553 or email cfsteam@mycfsgroup.com today to schedule a complimentary, no-obligation appointment with one of our wealth advisors.